There’s been a lot of talk in the jewelry and diamond industry about how to reach Millennials, a group of 77 million young American consumers – just under a quarter of the US population – who are finally reaching “jewelry buying” age. On paper, these young shoppers – born between 1981 and 2001 – look like great prospects for jewelers.

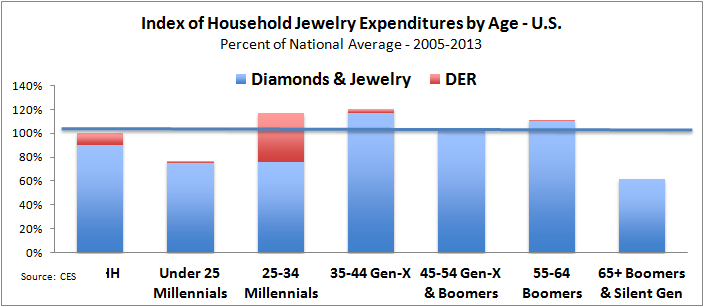

Not so fast, though: their jewelry expenditure numbers tell a different story. Millennials spend no more on jewelry per household than any other demographic generation including Gen-X and Boomers. And, when engagement ring sales are eliminated, Millennials’ jewelry expenditures are below the national average.

Here’s the punch line: based on both the latest data as well as decades of trends, household income is still, by far, the best predictor of a consumer’s likelihood to purchase diamonds and jewelry. All the other demographic factors – age, ethnicity, household size, location, education and others – simply aren’t very important.

Millennials look good on paper, but their spending doesn’t measure up

Marketers are always looking for new shoppers, and Millennials offer them an opportunity. These young consumers are newly employed and are looking for ways to spend their new-found money. Jewelers see lots of opportunity, for a variety of reasons:

Millennials are at the prime age for buying a diamond engagement ring. With an average ticket of near $4,000 for a diamond engagement ring, this high-dollar, but low-profit item is important to jewelry merchants, since it should lead to future jewelry purchases.

Many of those young shoppers are DINKS – Double Income, No Kids. Therefore, they should have discretionary income to spend on jewelry.

Millennials seem to be interested in fashion jewelry, a low-ticket, but high-profit category. Jewelers hope this will lead to bigger-ticket jewelry purchases in the future.

But these qualitative factors belie the truth: Millennials’ jewelry spending, on a per-household basis, is about the same as other generations of American consumers aged 25 through 65, as the graph below illustrates. When diamond engagement rings are eliminated from the equation (red portion of the bar for age 25-34 shoppers), Millennials’ jewelry expenditures (blue portion of the bar) are below average.

High-income households have most potential in US

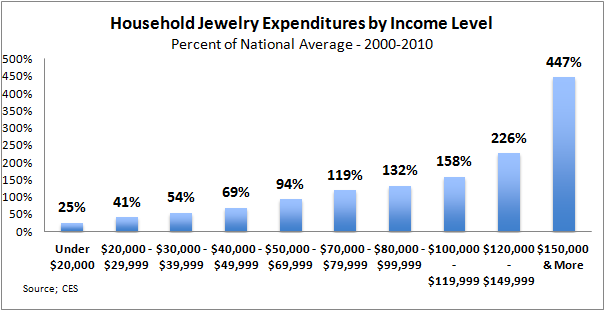

In the US market, roughly eight percent of the total households – about 9.5 million households – have an annual income over $150,000. Not only do these high-income shoppers spend more on jewelry, they spend a lot more than lower-income households. Their annual aggregate jewelry expenditures represent 25-to-30 percent of the total jewelry market in the US, or $20-to-23 billion per year.

If jewelers can identify that top tier of consumers – nearly one-in-10 households, they can capture more than one quarter of the total jewelry spending in the U.S.

The graph below illustrates jewelry expenditures for the decade 2000-2010, which includes the “Great Recession.” High-income shoppers kept spending on jewelry during that recession, while lower income consumers cut back substantially. The percentages shown on the bar graph illustrate the “percentage of the national average household expenditure” that each income group spends on jewelry annually. For example, high-income households – $150,000 or more annual income – spend 447 percent of the national average, or more than four times the average jewelry expenditure. In 2013, the latest data available, the typical US household spent just over $600 on jewelry, but high-income households spent close to $2,700.

Summary: those with the gold, spend on the gold

When infamous bank robber Willie Sutton was asked why he stole money from the banks, he answered, “That’s where the money is!”

Jewelers could take a lesson from Sutton: high-income consumers are by far the best customers for jewelers, because they have the discretionary income to spend on jewelry. In short, that’s where the “jewelry money” is.