The diamond industry is out of balance. The rough diamonds produced at mines only partially fit current consumer demand. This may explain why price movement is restrained. Meanwhile, among lab-grown goods, matters are a little more lively.

Although prices of smaller lab-grown goods have been mostly stable, the prices of larger goods sank in the first quarter of 2019. A combination of oversupply and technological developments contributed to the price decline. These two causes are also the biggest issues related to lab-grown.

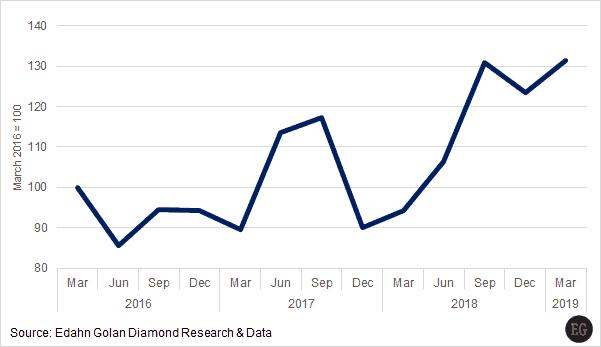

Inventories growing

Inventories of round-shaped polished natural diamonds held by wholesalers and manufacturers increased by more than 6% in the first quarter of 2019, as compared to the fourth quarter of 2018. The bulk of the increase was among quarter- and half-carats.

The overall rise in inventory levels adds to an already ongoing buildup in polished diamond stocks. On a year-over-year basis, inventory levels rose nearly 40%, the highest increase in three years, according to our research. This does not spell good news for the diamond industry on any level – production, manufacturing or financing.

Demands are specific and limited

The inventory buildup is not surprising in light of weakening demand. Although demand for natural diamonds expanded to a wider range of goods, the overall quantity in demand has declined both quarter-over-quarter and year-over-year.

An unenthusiastic trade show in Hong Kong and the very limited activity at Basel are two of the glaring examples of the level of demand in the market.

Another aspect of the change in demand for polished diamonds is the cautious approach taken by market participants: Retailers are holding as minimal a stock as possible, there is a rise in wholesalers’ willingness to offer goods on memo, manufacturers in India have reduced their polishing activity by an estimated 30% and De Beers has decided to reduce production.