The participants of the Kimberley Process (KP) established in 2000 in Kimberley at the initiative of South Africa, Botswana and Namibia are diamond producing and diamond importing countries, which pursue the aim to prevent trading in the so-called “conflict diamonds“ used for acquiring weapons and supporting anti-government and terrorist organizations. As of now, the KP has 54 participants, including the European Union, and since the latter comprises 28 member-states, the KP participants represent 81 countries.

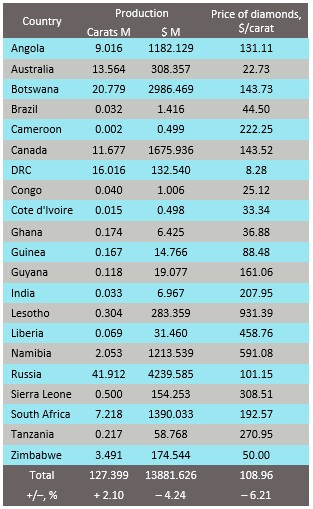

According to the data released by Kimberley Process, 21 countries contributed to global diamond production in 2015 (Table 1).

Table 1

Diamond production by country in 2015

Based on the Kimberley Process data in 2016

Preliminary analysis of the above data shows that, in spite of higher diamond production going up by 2.10%, the value of globally recovered rough decreased by 4.24% due to a price drop by 6.21%. The average price of diamonds stood at US$ 108.96 per carat.

The most expensive diamonds were mined in Lesotho (931.39 US$ per carat), as well as in Namibia, Liberia, Sierra Leone and Tanzania due to mining on alluvial diamond fields and artisanal production methods (excluding Namibia), when only large-size stones are mainly sought for and extracted.

The countries producing rough from ore mined at primary deposits value their diamonds much higher than the world’s average and the price in South Africa is US$ 192.57 per carat, in Canada it is US$ 143.52 per carat, in Botswana (where De Beers is running its operations) – US$ 143.73 per carat and in Angola – US$ 131.11 per carat. In Russia, the price of mined diamonds is slightly lower – US$ 101.15 per carat, due to different diamond ore dressing techniques. Russian concentration plants use autogenous tumbling mills for ore dressing to extract diamonds ranging from 50 to 0.5 mm in size, while mining operations outside Russia use multi-stage fragmentation permitting to recover diamonds larger than 1 mm and preserve them intact, especially larger stones (over 20 mm in size).

In the countries producing low-priced rough (at US$ 50 or less per carat) and having weak state control over diamond distribution, rough is repurchased by various middlemen at low prices and then sold at much higher prices on the market. The exception in this case is Australia, which has impact-type diamond deposits mainly yielding small-size diamonds.

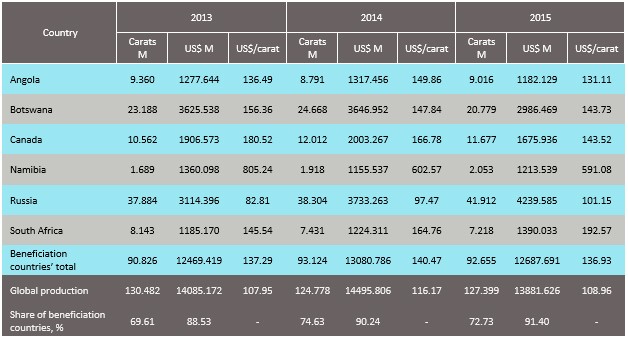

In 2014, Namibia joined the pool of countries producing rough diamonds worth more than $ 1 billion and practicing beneficiation, that is having diamond-cutting operations – Angola, Botswana, Canada, Russia and South Africa (Table 2).

Table 2

The table is based on the Annual Global Summary data: 2013, 2014, 2015 Production, Imports, Exports and KPC Counts

As it can be seen from the above data, the beneficiation countries play a pace-setting role in the global diamond business, producing more than 70% of diamonds by volume and already over 90% by value, which indicates a higher level of organization in their diamond trade on the backdrop of progressing diamond cutting industries.

Yuri Danilov, Ph. D., Director of “Expert” Information and Analysis Center at Ammosov North-Eastern Federal University