The diamond mining sector is under pressure with production rising to peak levels at a time when rough sales are slumping and polished demand is sluggish. The major miners are holding above-average inventory that they have pledged to release slowly in an attempt to avoid over-supply to a market struggling in the face of its current downturn.

If there is one thing the industry needs right now, it is a measured approach in the release of rough supply – at prices that reflect polished demand – to ensure stability and profitability for manufacturers and rough dealers.

It appears that the miners are maintaining a cautious outlook for the year even as rough demand spiked in January and remained firm in February. “We’re selling what our customers want and need rather than doing anything that might not be in ours or the industry’s best interests,” Gareth Mostyn, De Beers head of strategy, recently told Bloomberg. “The key is to continue to build confidence through 2016.”

However, there are concerns about the rough held in the mining companies’ vaults. After all, the current downturn resulted from an oversupply of polished as manufacturers bought rough at higher prices in 2014 to satisfy Chinese demand that didn’t materialize. As polished inventories now diminish, there has been a build-up of rough inventory in the mining sector as the majors hold back supply to align with lower demand.

ALROSA, Rio Tinto on the rise

That begs the question what are miners doing with unsold rough and whether output needs to be curbed? It’s not such a simple question as many factors are taken into consideration, particularly by the majors.

For example, now might be a good time to operate a mine as production costs are lower due to declining diesel costs and favorable exchange rates in South Africa and Russia. The Botswana government, which owns 15 percent of De Beers and has a joint venture with the company in the Debswana mining division, might need to maintain certain levels of production as diamond output is an important factor in its gross domestic product (GDP) growth calculation.

De Beers structure is also such that its selling division buys from its mining division as per sightholder demand. Therefore, the bulk of De Beers inventory is more likely being held at Debswana and is not readily available at its Global Sightholder Sales unit.

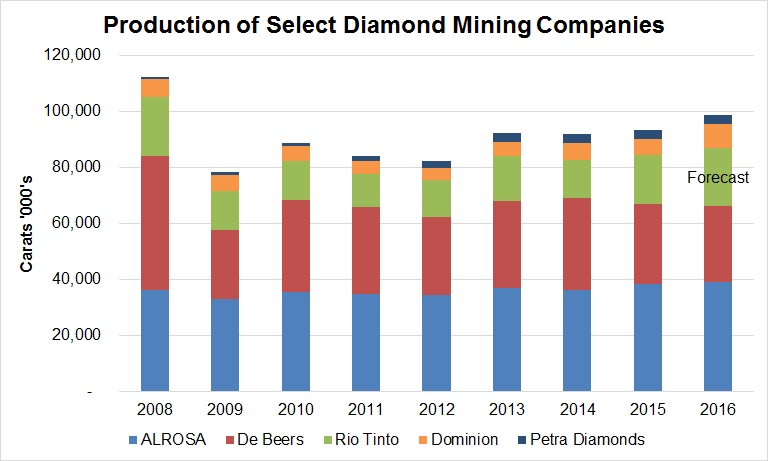

Still, De Beers was the only one of the top three miners that reduced production to align with a drop in demand in 2015 and the company has further adjusted its outlook for 2016. ALROSA and Rio Tinto both registered production increases last year and are forecast to ramp up output again this year.

The combined output of ALROSA, De Beers, Rio Tinto, Dominion Diamond Corp., and Petra Diamonds – which account for an estimated 75 percent of global production by volume – increased 2 percent in 2015 and is projected to rise about 6 percent in 2016 (see graph).